The 2015 storm season is officially underway. The experts at Colorado State University have released their forecast, calling for a below-average hurricane season in the Atlantic this year. Between now and November 30, we can expect seven named storms. Of those, three will likely become hurricanes and one will reach major hurricane strength with sustained winds of 111 miles per hour or greater. While the news of a below-average storm season is welcome news, we should not become complacent. Even a moderate hurricane can cause severe damage. And of course, the summer months also bring tornadoes, wildfires, droughts, thunder, lightning and rain storms. So it’s time to refresh the drill, update the “go-kit” and make sure all of your business continuity preparations are up to date. The increased news attention focused on severe weather offers the opportunity to remind your employees, family members and suppliers of basic preparation measures. So now is the time to do it.

Posts Tagged ‘Hurricanes’

The 2015 Storm Season Has Begun

Monday, June 1st, 2015Mildest Hurricane Season Since 1982

Monday, October 26th, 2009

2009 Is Lucky So Far

Since June 1, the official start of the Atlantic storm season, only two hurricanes have formed, making this the mildest hurricane season since 1982, which also saw only two hurricanes. This year, eight tropical storms strengthened to be named storms, the lower number since 1997, but only one storm, Claudette, made landfall in the U.S. Claudette formed in the Gulf of Mexico and struck the Florida panhandle on August 16 and 17. No hurricanes made landfall in the U.S. this season to date. Still, the National Hurricane Center in Miami advises us not to become complacent as the hurricane season does not officially end until November 30. Nevertheless, the peak hurricane season occurs from late August until mid-October, so the worst may be behind us for 2009. The U.S. may have benefited from the “El Niño” climate phenomenon in which warmer waters in the Pacific Ocean produce weather patterns that create wind shear in the Atlantic Ocean. The wind shears, strong winds blowing from different directions at different altitudes, can tear apart tropical waves emerging from the African coast that can develop into hurricanes.

The respite is surely welcome in the Gulf Coast states, which are still recovering from a very active hurricane season in 2005, when the National Hurricane Center ran through the alphabet in naming 28 tropical storms. A spokeswoman for the Property Casualty Insurers Association of America stated that insurers will use 2009 to rebuild their claims reserves after paying out more than $90 billion over the past decade in connection with hurricane losses. The break is particularly welcome for small businesses that would have difficulty budgeting for hurricane-related evacuations in this difficult economy. However, we should also remember that while hurricanes provide graphic imagery on television, it was a tornado that killed 21 people in Central Florida on February 2, 2007. As always, we must be ready for the everyday disaster to build resilience for the more serious ones.

Protecting New York City From the Sea

Sunday, May 31st, 2009

New York City Sea Barriers

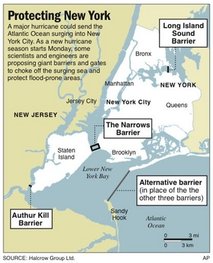

I had the opportunity to tour the emergency response center of New York City’ s Office of Emergency Management. Officials there told me that one of their greatest concerns was the threat of a major hurricane striking the city. Indeed, National Hurricane Center Director Max Mayfield testified before Congress “it is not a question of if a major hurricane will strike the New York area, but when.” A hurricane would flood Wall Street, the financial district, densely packed neighborhoods and the City’s infrastructure, which is largely underground, such as the subway. So I was very interested to learn of a conference held in advance of the new hurricane season (which starts on Monday) in which innovative solutions for New York were presented.

Some engineers are proposing the construction of a barrier to block the sea surges and protect areas vulnerable to flooding. One idea involves the construction of a barrier between New Jersey and Queens, some five miles long, which would rise out of the water to meet storm surges. It may sound extreme, but if New York were to experience a repeat of the hurricane that struck Long Island in 1938, the storm surge would be as high as 25 feet in parts of New York City. The result would be flooding of as many as 600,000 homes and an evacuation of three million New York residents. The economic losses would exceed $100 billion. This makes the cost of the barriers, estimated to be $6 – $9 billion, appear to be a sensible investment. Of course, at this time New York doesn’t have the finances for such an investment and seeking help from the federal government would not appear to be a prudent strategy. Surely every community would rightly demand the same protection. For the time being, it make sense to prepare for flooding by moving critical infrastructure such as pumps to higher elevation areas. It also makes sense to launch a public awareness campaign. When I toured OEM’s command center, I learned that their leadership feared New York residents would enter subway stations on a storm alert – the last place you want to be when a hurricane or flood is forecast.

Two Months Remain in the 2008 Hurricane Season

Wednesday, October 1st, 2008

Still at risk in October

There are two months remaining in the 2008 hurricane season and researchers at Colorado State University expect twice the hurricane activity during the month of October 2008 relative to past years. The reason for the forecast of exceptional activity is low sea-level pressures and warm sea-surface temperatures across the tropical Atlantic, a bad combination for severe storms.

By the way, the captioned photograph is one I had taken at a small business conference in Florida. I had just given a talk on hurricane preparedness and decided to unwind a bit by walking along the promenade in the unusually mild weather. But I could have used a photograph of a colder climate, as Canada was recently pummeled by Hurricane Kyle. In the second edition of Prepare for the Worst, Plan for the Best: Disaster Preparedness and Recovery for Small Businesses (Wiley, 2008), I cited the evacuation of Newfoundland when Hurricane Juan moved up the Atlantic Coast. Kyle caused problems for Nova Scotia and thereafter I was asked to contribute a bylined article to the Daily Business Buzz of the Nova Scotia Business Journal. The Toronto Globe and Mail also advised its readers of our book. So expect some nail-biting from Canada to Florida during the month of October as meteorologists monitor Atlantic storm activity.

Thinking of Texas at This Time

Thursday, September 11th, 2008

Annual Conference in Houston

As the Gulf Coast of Texas mounts an evacuation in anticipation of Hurricane Ike, I am reminded of my last visit to that area. The occasion was a series of workshops I delivered on small business disaster preparedness for the Small Business Development Centers in San Angelo, El Paso, Laredo and San Antonio. It was a coming home of sorts for me because I was first introduced to the ASBDC network when I spoke at their annual conference in Houston in 2006. The local events in Texas were fantastic and attended by the mayors of the cities, the chiefs of police and fire services, presidents of the local Red Cross chapters, commissioner of public health and other officials. One of the points that was made very clearly was that over the course of a 30-year mortgage, you have a 26% chance of a flood versus a 9% chance of a fire. In addition, in any given year, 30% of the homes and businesses that flood are in areas that have never before experienced a flood. This is an alarming figure, because many homeowners and small business owners mistakenly believe that their insurance policies cover flood damage and they don’t (you have to purchase flood insurance separately).

This is a major source of concern for state insurance commissioners. I was recently interviewed on The Family Breakfast Show of WICC-AM to discuss flood risks for small businesses. The following day, the scheduled guest for the program was the insurance commissioner of Connecticut, as in the aftermath of Tropical Storm Fay, there is a need to educate the public about flood risks.

The other significant challenge that Texas faces is that for evacuees, all roads lead to San Antonio. At these workshops in 2007, emergency officials discussed the likelihood that as many as 1.5 million Texans may have to be evacuated from the Gulf Coast area in anticipation of a major hurricane. However, San Antonio has only 30,000 beds available in its entire hotel and hospitality industry. In Prepare for the Worst, Plan for the Best, I had discussed my work with Peg Callahan and Deidre Patillo of the San Antonio Small Business Development Centers. They are certainly in my prayers at this difficult time.

Baton Rouge Small Businesses Post-Gustav

Thursday, September 11th, 2008

This way to escape the hurricane

On Monday, September 8, I was a guest on the Jim Engster program of WRKF, the National Public Radio Station in Baton Rouge. You can click this link if you would like to hear the podcast of the interview. The topic was what Baton Rouge small businesses need to do to accelerate their recovery from Hurricane Gustav. The following are the tips I discussed with Jim Engster:

1. Rapid response is critical. Many small business owners will be in a state of shock and disbelief as a consequence of the disaster. However difficult it may be, they must manage their emotions and work to restore operations as soon as possible. The choice is not whether to recover quickly or whether to recover at a more measured pace. The choice is whether to recover quickly or not to recover at all. A study of small businesses affected by the 1993 World Trade Center bombing found that of those businesses that could not restore operations within five business days, 90% of them were out of business within one year. Prioritize your business needs according to relative urgency and delegate where necessary.

2. Mitigate your losses. To establish a valid property insurance claim, you must demonstrate to your insurer that you acted in good faith to mitigate your insured losses. Consider a hypothetical example. Let’s imagine that you have returned to your property and you see broken glass about the site. You must take reasonable steps to insure that people will not be injured by the broken glass. Insurance companies are not very tolerant of passive policyholders who fail to act in their interests to limit losses. Limit subsequent losses to your business by taking prudent steps, such as restoring fire sprinklers or other equipment that may have been damaged by the storm.

3. Identify your implicated policies. You should invest the time and effort required to examine all insurance policies implicated in the disaster, rather than foreclose options for coverage by limiting the scope of your review. Begin with insurance policies for first-party property losses that cover direct property damage, including collateral damage and indirect property damage, such as business interruption losses and loss-related expenses. Next review all-risk policies, named peril policies, business owner’s policies, policies covering particular endorsements, valuable papers and records policies.

4. Provide timely notice. Your business owner’s policy likely requires you to provide timely notice to your insurance company of covered losses. Do not forfeit indemnification for a covered loss by failing to give timely notice. If you are in doubt as to whether an item is covered by your policy, err on the side of caution and include it in your claim.

5. Report the facts, don’t diagnose the cause. Think of the words of Sergeant Joe Friday, “Just the facts, ma’am”. Here is an example of why you should not be a diagnostician. A sole proprietor worked from her home near the World Trade Center on 9-11 and experienced a systems crash. She concluded that the crash was most likely due to the loss of electrical power that was the result of the terrorist attack and so notified her insurer. Because her policy did not include an endorsement for interruption of electrical supply, that portion of her claim was denied. In fact, the damage to her computer was the result of soot and ash clogging the fan of her computer, a peril that was covered by her policy. The denial of coverage and dispute that followed could have been avoided had she sent a description of the problem without the diagnosis. Had the insurance adjuster inspected the damaged computer, he would have seen the soot and ash in the machine and likely authorized payment on the claim. Her hasty diagnosis resulted in a denial and delay of her claims payment.

6. Inspect your IT and other electronic assets at least twice to ensure that you have not overlooked anything. I began hearing unpleasant grinding noises emanating from my PC when I returned to my office following the 9-11 disaster. I suspect I had not heard them earlier because of the background noise outside my office as work was being done to restore electricity and other essential services. Upon closer examination, I learned that the noise signaled an imminent hardware failure. By inspecting each IT asset twice, I avoided the error of submitting an incomplete claims report.

7. Document your loss mitigation and other loss-related expenses; your business owner’s policy likely covers them. Such expenses might include overtime wages paid to employees who work to restore the business, lease payments for alternate office facilities when your primary space has been rendered unusable by the hurricane, costs of purchasing assets for temporary business use and so forth.

8. Get help if you need it. You are likely to experience a range of emotions following a disaster, from disorientation to shock and disbelief to grief and mourning. This is not uncommon and may continue for some time after the disaster. You won’t be able to look after your employees and family if you are run down. Get the support you need.

9. Assess your performance. Unfortunately, Gustav may not the last hurricane of the 2008 season. Review your business contingency plan and, in particular, your employee training to identify areas for improvement so you will be better prepared for the future. You can and will learn from this difficult experience.

10. Exercise care when negotiating continued insurance coverage. Premium increases following a major disaster are not uncommon, but there are steps you can take to protect yourself. In particular, be aware of the “paying more/getting less” phenomenon in which increases in insurance premiums can be dampened by excluding risks that had previously been covered. Also, be prepared to demonstrate to your underwriter the features of your business protection plan that make your business a better risk.

Dodging a Bullet, But Still Suffering

Thursday, September 11th, 2008

Appreciation from the Red Cross

Having feared the worst, residents of Louisiana got a reprieve, of sorts, when Hurricane Gustav did not leave a trail of devastation comparable to that of Hurricane Katrina. This has caused problems of another kind; Gustav is still a serious disaster and residents in the affected areas are in need of assistance. But charitable giving has not kept pace with the need, in part because of distorted perceptions from catastrophizing risk. The fact that Gustav was not as powerful as Katrina offers little comfort to Louisiana residents living in emergency shelters until their power and other services are restored and they can safely return home. To meet the needs of those who have been displaced by Gustav, the Red Cross has taken on debt, in the hope that donor contributions are on the way (that report from the Washington Post).

On the occasion of my most recent visit to New Orleans, I was surprised with a Certificate of Appreciation from the Gulf Coast Recovery Director of the American Red Cross. This was an acknowledgement of the contributions that my own small business has consistently made over the past few years. I am currently working out the details of a promotion in which profits on the sale of my book will assist disaster relief efforts. I urge other small businesses to join in; helping the relief efforts is not only a worthwhile thing to do, it can be effective team and skill building for your own organization. This has been a tough year in the United States for major natural disasters; in addition, to a severe hurricane season, we have had tornadoes in the southern states, floods in the midwestern states and wildfires in California. The need is certainly there.

Louisiana Small Businesses Dare to Prepare

Thursday, September 11th, 2008

Louisiana SBDC Disaster Kit

As residents of Louisiana anticipate the approach of Hurricane Gustav, I am reflecting on my most recent trip to the Louisiana Gulf Coast. The occasion was a series of “Dare to Prepare” workshops sponsored by the Louisiana Small Business Development Centers in mid-August. The workshops received very kind attention from the New Orleans Times-Picayune. Participants in the workshops were given a number of takeaways, including a disaster kit. One of the participants in the second workshop in Slidell, Louisiana announced to the group that she had worked at 225 Broadway in Lower Manhattan on 9-11-01. Having lost her job, she moved to London and then re-joined her family in New Orleans to help with their business, just in advance of Hurricane Katrina. She and her sister were seated in the front row at the workshop, eager to share their experiences of disaster recovery and preparing for the next one. I cannot think of a better example of resilience and like all Americans, I am praying that Hurricane Gustav spares the Gulf Coast.