Follow the Fortunes

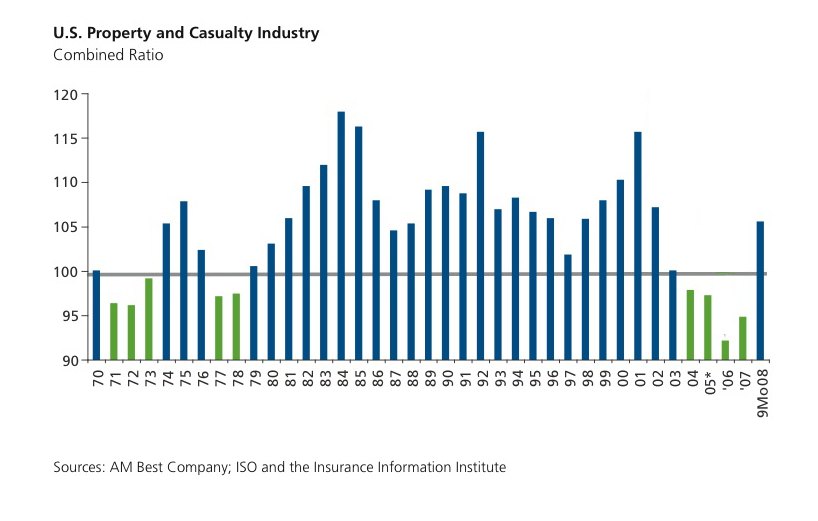

In a previous entry, I wrote about anticipated increases in property-casualty insurance premiums. Reinsurance broker Guy Carpenter, published a report Cats and Credit Push Prices Up: Global Reinsurance Review January 2009 in which it found that property casualty rates rose only 11% across the United States this year. You may wince at the word “only”, but this rate increase is dampened as compared with what followed Hurricane Andrew in 1992, the terrorist attacks of September 11, 2001, and Hurricanes Katrina, Rita and Wilma in 2005. This is remarkable given the level of catastrophes (close to $20 billion in insured losses) in 2008 and the financial losses on the investment portfolios of insurance companies. The rate hikes could have been much, much worse. What typically happens after two or three annual renewal seasons of increasing rates is that the Fortune 500 will seek alternative means of financing their risks at lower costs. This might include self-insurance through corporate captives, for examples. Four states – Michigan, Missouri, Louisiana and Connecticut – are enacting legislation similar to the statutes in Vermont to establish captive insurance companies in their jurisdictions or to persuade existing captives to re-domicile. The recent announcement of President Obama concerning increasing scrutiny of offshore corporate vehicles (corporate captives are commonly found in places like Bermuda and the Cayman Islands) may accelerate this trend. What this means is that supply and demand will eventually favor the small businesses. As large corporate insureds withdraw from the expensive primary insurance market in favor of less expensive alternative risk financing vehicles, demand declines and price follows. Small businesses can then purchase their insurance at lower costs. In other words, sit tight, Fortune 500 companies will soon look to cut their insurance expenses and we will benefit from the lower prices that follow their actions.