The small business section of the New York Times published an article titled “Buying the Best Insurance for Your Business.” I was among the experts quoted in a piece focusing on business interruption insurance. Too often small business owners focus on property damage and overlook the need to protect against revenues lost when disaster strikes. The article reports that the owner of a beauty company whose business experience a fire learned this lesson the hard way. The article also provides helpful tips on purchasing general liability and workers compensation insurance.

The small business section of the New York Times published an article titled “Buying the Best Insurance for Your Business.” I was among the experts quoted in a piece focusing on business interruption insurance. Too often small business owners focus on property damage and overlook the need to protect against revenues lost when disaster strikes. The article reports that the owner of a beauty company whose business experience a fire learned this lesson the hard way. The article also provides helpful tips on purchasing general liability and workers compensation insurance.

Archive for the ‘Insurance companies’ Category

Buying the Best Insurance for Your Business

Sunday, December 20th, 2009Health Insurance Reform a Double-Edged Sword

Thursday, July 2nd, 2009Regulatory reform often has unintended consequences; the current debate over health insurance reform is no exception. With proposed government subsidies, as many as ten million low-wage employees may choose to drop their employer-provided health insurance and purchase coverage on the open market. With such attrition rates, small businesses may find their group purchasing power reduced, making it more expensive to insure the remaining employees. This could draw another ten million employees into the individual market, if small businesses are forced to drop their coverage plans due to the crowding out effect of the government exchange. According to a survey of the National Small Business Association, nearly 10% of small business owners are contemplating dropping their medical insurance coverage next year. The uncertainty around health care reform makes a lengthy debate expensive, with the cost falling disproportionately on small businesses.

Is Anyone Surprised, Really?

Sunday, June 14th, 2009

The View From My Office Window

In the first edition of Prepare for the Worst, Plan for the Best: Disaster Preparedness and Recovery for Small Businesses (John Wiley & Sons, Inc., second edition, paperback, August 2009), published in 2002, I wrote that you should consult with professional and trade associations and others in the small business community to learn of their experiences in selecting an insurance carrier. Certain companies have good reputations of service in the small business market, while others are best avoided. I also wrote that there were two insurance companies that were particularly difficult to deal with for Lower Manhattan small businesses to get their 9/11-related claims paid. So I was not altogether surprised to read in the news media that “AIG was playing hardball on paying claims” to the passengers of USAirways Flight 1549. Could it be argued that AIG’s tough stance on claims relates to its present financial difficulties?

Nope.

In the current edition of the book, I shared the experience of “Ariel Goodman, whose small business was based in the World Trade Center. Ariel also lived in an apartment building directly facing the World Trade Center. Following the terrorist attacks, the Department of Health condemned her apartment building. What was doubly unfortunate was that her business records were backed up at her home and her personal records were backed up at her office. Within the space of a few minutes, she lost both simultaneously…Ariel, by the way, founded From the Ground Up, a nonprofit association of Lower Manhattan small businesses affected by 9/11.” Ariel needed her commercial insurance policy to file her claims. Obtaining a copy from her accountant was not an option, as her accountant’s office was also located in the World Trade Center and he had not thought to back up his records offsite. Her insurance company denied her commercial claims and when she sought to protest their decision, repeatedly refused her requests over several months to furnish her with a copy of her policy. I advised her to send a copy of her written request to the New York State Insurance Commissioner, to make the regulators aware of her struggle with her insurance company. That did the trick.

You already guessed it: her insurance company was AIG.

That, in my opinion, is the problem for AIG. Aviation insurance is an anomaly in that insurers are typically not obligated to pay claims unless there is proof of negligence on the part of the airline. In this case, no finding of negligence has been made. At the same time, because of the sheer size of potential aviation liability claims, such coverage is typically syndicated among a group of insurers with one insurer acting as the lead underwriter. If the lead insurer pays claims that it is not obligated to pay, it faces problems of its own with the other insurers in the syndicate. An insurance company with a pristine reputation might be able to explain this phenomenon to angry passengers. They could show how paying claims that they are not obligated to pay raises the cost of coverage for everyone. It is just that if there are those who believe that the insurance company knowingly denies legitimate claims and then, on top of that, owes its continued existence to a massive taxpayer bailout of the reckless behavior of its senior executives, well, don’t expect much sympathy.

Business Owners Policies and the Recession

Friday, June 5th, 2009

Not the Business to Be In Right Now

MarketStance, a research firm that provides analytics to the insurance industry, offered an unusual perspective on the significance of the recession for smaller businesses. They report that “the depth and duration of the current recession, when combined with the financial crisis and current soft market conditions, represents a perfect storm of unique proportions for the commercial lines industry.” In an earlier blog posting, I explained how the dual threats of poor underwriting results (due to high catastrophic insured losses in 2008) and poor investment performance signaled rising rates for insurance. Cash flow underwriting, a strategy for profitability in which returns on the investment portfolio compensate for underwriting losses, no longer works in this market. Insurers have the choice between hunkering down and waiting for the cycle to turn or proactively managing their books of business to try to reposition for profitability. MarketStance believes that $600 million of business owner policy premiums will be lost through year-end 2010 as a consequence of the recession. These losses will result from both business failures and declines of surviving businesses in recession-sensitive segments of the small business sector, such as the construction industry. But over the same time frame, four times as much new premium potential will emerge from new business formation and growth, more than offsetting the losses due to the recession. The white paper published on MarketStance’s website, presenting an analysis of the business owners policy market, is really about the possibilities of entrepreneurship and creative destruction.

Their research found that 60% of the small business market, roughly $14 billion in written premiums, is experiencing significant stress due to the recession. Not surprisingly, this varies significantly by region, with states such as Arizona and Michigan faring worse than average. But states such as Nevada and Florida are doing much better than average, notwithstanding their experiences with the construction boom and subprime mortgage crisis. Other states, such as Texas, Alabama, North Carolina and Maryland, have more broadly diversified economies, with most of their small businesses working in either growth areas or at least areas that are not tied to the economic cycle, such as tourism. For policymakers, this report offers an instructive lesson on the benefits of economic diversification. For small business owners, it is a lesson on the importance of choosing a suitable business niche. But recession-sensitive or not, all small businesses must prepare for what will likely be a challenging insurance renewal season.

Without Precedent!

Wednesday, May 27th, 2009

Unusual Case

In Prepare for the Worst, Plan for the Best: Disaster Preparedness and Recovery for Small Businesses (John Wiley & Sons Inc., second edition, 2008), I wrote that the cash flows of an insurance operating company could not be diverted for other corporate purposes, thus providing some security for the policyholders. Last week, lawyers representing a group of policyholders of American International Group Inc. (AIG) filed a lawsuit in California Superior Court against the company, its executives and its auditor, PricewaterhouseCoopers. The policyholders allege that AIG had improperly diverted capital from its insurance operating companies, thereby undermining the critical asset for claims payment. State insurance commissioners are supposed to prevent this from happening; specifically, holding companies cannot extract capital from their insurance subsidiaries, no matter how much pressure they are under. However, the policyholders who are plaintiffs in this lawsuit alleged that AIG had pledged the cashflows of its insurance subsidiaries to repay the Federal Reserve Bank for the government bailout funds. This is absolutely without precedent and raises some troubling questions with respect to the regulatory responsibilities of the state and federal governments. I will be following this case with great interest.

Sit Tight and Follow the Fortune 500

Friday, May 8th, 2009

Follow the Fortunes

In a previous entry, I wrote about anticipated increases in property-casualty insurance premiums. Reinsurance broker Guy Carpenter, published a report Cats and Credit Push Prices Up: Global Reinsurance Review January 2009 in which it found that property casualty rates rose only 11% across the United States this year. You may wince at the word “only”, but this rate increase is dampened as compared with what followed Hurricane Andrew in 1992, the terrorist attacks of September 11, 2001, and Hurricanes Katrina, Rita and Wilma in 2005. This is remarkable given the level of catastrophes (close to $20 billion in insured losses) in 2008 and the financial losses on the investment portfolios of insurance companies. The rate hikes could have been much, much worse. What typically happens after two or three annual renewal seasons of increasing rates is that the Fortune 500 will seek alternative means of financing their risks at lower costs. This might include self-insurance through corporate captives, for examples. Four states – Michigan, Missouri, Louisiana and Connecticut – are enacting legislation similar to the statutes in Vermont to establish captive insurance companies in their jurisdictions or to persuade existing captives to re-domicile. The recent announcement of President Obama concerning increasing scrutiny of offshore corporate vehicles (corporate captives are commonly found in places like Bermuda and the Cayman Islands) may accelerate this trend. What this means is that supply and demand will eventually favor the small businesses. As large corporate insureds withdraw from the expensive primary insurance market in favor of less expensive alternative risk financing vehicles, demand declines and price follows. Small businesses can then purchase their insurance at lower costs. In other words, sit tight, Fortune 500 companies will soon look to cut their insurance expenses and we will benefit from the lower prices that follow their actions.

Cash Flow Underwriting

Monday, May 4th, 2009

Harder Markets Ahead

In Prepare for the Worst, Plan for the Best: Disaster Preparedness and Recovery for Small Businesses (John Wiley & Sons Inc., second edition, 2008), I explained the cash flow of an insurance company (page 178):

“An insurance company collects premiums from its policyholders. such as your small business. It invests these premiums in assets, such as high-quality bonds and blue chip stocks, to earn investment income. It pays out expenses, such as premiums for its own reinsurance coverage, salaries to employees and so forth. It also pays claims to its policyholders for insured losses, or damages. The cash flow of an insurance company (premiums plus investment income less expenses less losses) is often expressed in terms of a combined ratio. The combined ratio is the sum of the loss ratio plus the expense ratio. A loss ratio of 100%, for example, means that for every dollar the insurance company collected in premiums, it paid out one dollar in losses and expenses. An insurance company with such a loss experience stays in business by engaging in so-called cash flow underwriting; that is, its insurance losses are more than offset by the investment income the insurance company earns on its premiums. In 1999, for example, insurance companies were paying out $1.07 in claims and expenses for every dollar collected in premiums. You can appreciate how sensitive the insurance industry is to the financial markets.”

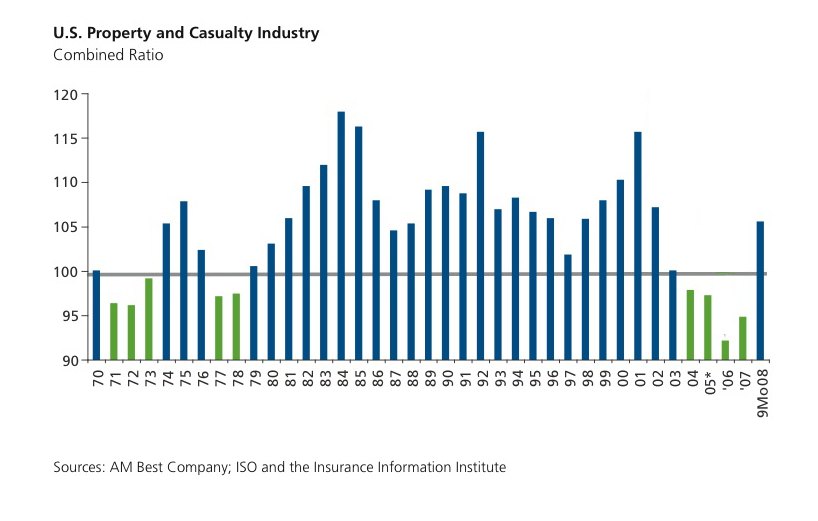

When the combined ratio becomes unsustainably high, the insurance industry can no longer rely on cash flow underwriting and has to raise premiums. Insurance industry professionals refer to this as a “hard market”, one in which rates are rising. This graph here shows the combined ratio for the U.S. property-casualty insurance industry from 1970 through the third quarter of 2008. The horizontal grey line shows the combined ratio at 100%, that is when the insurance industry breaks even. The bars that extend above the grey line are shaded in blue and show when the insurance industry is underwriting risks at a loss and relying on investment income to remain profitable. The green bars are those that do not reach the grey line; that is, the combined ratios are below 100% and the industry is making underwriting profits.

The insurance industry had a particularly difficult year in 2008: for the first three quarters of last year, the U.S. property-casualty industry paid $19.9 billion for catastrophic losses. These losses occurred at a time when the financial markets were in decline, and so investment income was insufficient to compensate for underwriting losses. Hence, the bar for the first three quarters of 2008 is blue in color, extending above the grey line for a 100% combined ratio. This suggests that the insurance market is about to become “hard”, cash flow underwriting is about to end, and premiums will rise. Better to renew your insurance coverage sooner rather than later, as later it will likely be more expensive.

Neatness Counts

Saturday, May 2nd, 2009

Get It Together

When I had to submit insurance claims against both my homeowner’s and commercial policies, the insurance staff who processed my claim remarked that mine was the best organized submission that they had seen – and so processing my claim jumped to the front of the queue! That is not surprising: which would you rather deal with – the well-organized claim submission, neatly presented with supporting documentation or the hastily assembled report that will take some time to decipher? Make life easier for the person you are dealing with and you will make life easier for yourself.

Now I have another insight to support this recommendation. I recently met with an executive of one of the five largest property-casualty insurance companies in the U.S. and he told me that when he had started his career ten years ago, 40,000 monthly claims were processed by 8 claims adjusters. This business function was automated such that 1.5 million monthly claims are now processed by 12 claims adjusters. Often a human eye never sees the claim. Another reason to make your submission legible and your life easier.

Unintended Consequences

Friday, March 27th, 2009

Bureaucratic Interference

In Prepare for the Worst, Plan for the Best: Disaster Preparedness and Recovery for Small Businesses (Wiley, second edition, 2008), I sought to explain the economics of the insurance cycle. Cash flow underwriting was, until recently, one of its defining features. Cash flow underwriting essentially involves pricing risks below the actuarially expected losses with the expectation that gains on the investment portfolio will bring the insurance operation to profitability. In essence, insurance companies collect premiums from underwriting risks and invest those premiums from which to pay claims and expenses. In the first edition of the book, I advanced the controversial argument that insurance premiums rose dramatically following 9/11, in part, because insurance premiums had been too low. High rates of return in the stock and bond market allowed insurance companies to underwrite business below the actual price of risk. The advantage of doing so was to preserve or gain market share in an environment where insurance was viewed as a commodity and providers competed almost exclusively on the basis of price. The downside to this practice of course, is that we have more volatility in the pricing of insurance risks, particularly commercial insurance and we have to think more carefully about the solvency of insurance companies with these pricing for market share strategies. Unlike the discount retail store, which closes a transaction with the sale of the product, the insurance company has to remain in business for years or decades to come to pay future claims.

Now with the federal government bailout of AIG, we have an interesting situation in respect of the cash flow underwriting dilemma. According to the Wall Street Journal, at a recent meeting with Federal Reserve Chairman Ben Bernanke, insurance executives complained that AIG was using its federal government money to cut prices and buy market share, thereby harming competitors and destabilizing the industry. Of course, as small business owners, we all want low prices, but we also want financially solvent insurance carriers. The federal government bail out of AIG introduced an element of moral hazard that our policymakers failed to anticipate. Of course, AIG may be responding to market pressure to retain business in the face of uncertainty about its future. But should their insurance premiums be inadequate to cover their insured risks, the stage is set for yet another bailout and a very vicious circle for taxpayers and policyholders alike. It is an insightful article and I commend the Wall Street Journal for its reporting.

Don’t Scare the Policyholders

Tuesday, March 10th, 2009

The escalating cost of bailing out financial conglomerate American International Group (“AIG”) is staggering. Last week, Federal Reserve Chairman Ben Bernanke testified at a Senate Budget Committee hearing that AIG, which has recently benefited from multiple government rescues, made him “angry” because it had made “huge numbers of irresponsible bets” and “was a hedge fund, basically”. He reported that AIG’s investment vehicles lacked oversight. Last week, AIG confirmed it would give the US government a large stake in its two largest divisions as part of a more than $30 billion rescue package for the company, which lost nearly $100 billion in 2008. The Federal Reserve Chief defended the bailouts on the ground that as the world’s largest insurance company, AIG was too big to fail. In fact, the insurance operations of AIG that serve policyholders for property casualty, health and life insurance are regulated and presumably adequately reinsured and reserved for expected claims. It was the non-insurance financial businesses of AIG, in particular AIG Financial Products which took extraordinary risks on credit default swaps, that caused the fiancial losses of the company. Our policymakers should be clear in their use of language to avoid misleading the public as to what is really at risk here. And as economist Nouriel Roubini reported, this current round of bailouts for AIG was for the benefit of the large banks that were counter-parties to the aggressive financial trades made by AIG Financial Products. One would have thought that sophisticated Wall Street institutions would have diversified their risks to limit their exposure to any single counterparty and would have set aside allowances for expected credit losses. It is disingenuous to pretend that the bailout actions are being taken to protect the integrity of our financial system.