Harder Markets Ahead

In Prepare for the Worst, Plan for the Best: Disaster Preparedness and Recovery for Small Businesses (John Wiley & Sons Inc., second edition, 2008), I explained the cash flow of an insurance company (page 178):

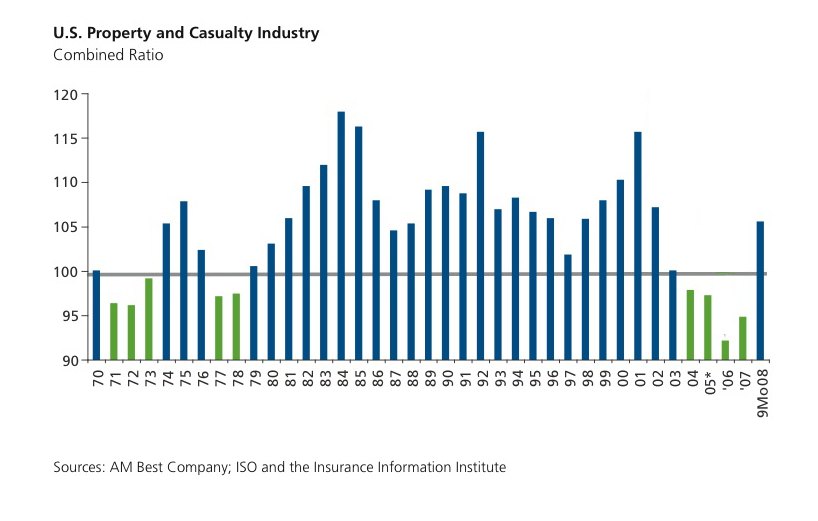

“An insurance company collects premiums from its policyholders. such as your small business. It invests these premiums in assets, such as high-quality bonds and blue chip stocks, to earn investment income. It pays out expenses, such as premiums for its own reinsurance coverage, salaries to employees and so forth. It also pays claims to its policyholders for insured losses, or damages. The cash flow of an insurance company (premiums plus investment income less expenses less losses) is often expressed in terms of a combined ratio. The combined ratio is the sum of the loss ratio plus the expense ratio. A loss ratio of 100%, for example, means that for every dollar the insurance company collected in premiums, it paid out one dollar in losses and expenses. An insurance company with such a loss experience stays in business by engaging in so-called cash flow underwriting; that is, its insurance losses are more than offset by the investment income the insurance company earns on its premiums. In 1999, for example, insurance companies were paying out $1.07 in claims and expenses for every dollar collected in premiums. You can appreciate how sensitive the insurance industry is to the financial markets.”

When the combined ratio becomes unsustainably high, the insurance industry can no longer rely on cash flow underwriting and has to raise premiums. Insurance industry professionals refer to this as a “hard market”, one in which rates are rising. This graph here shows the combined ratio for the U.S. property-casualty insurance industry from 1970 through the third quarter of 2008. The horizontal grey line shows the combined ratio at 100%, that is when the insurance industry breaks even. The bars that extend above the grey line are shaded in blue and show when the insurance industry is underwriting risks at a loss and relying on investment income to remain profitable. The green bars are those that do not reach the grey line; that is, the combined ratios are below 100% and the industry is making underwriting profits.

The insurance industry had a particularly difficult year in 2008: for the first three quarters of last year, the U.S. property-casualty industry paid $19.9 billion for catastrophic losses. These losses occurred at a time when the financial markets were in decline, and so investment income was insufficient to compensate for underwriting losses. Hence, the bar for the first three quarters of 2008 is blue in color, extending above the grey line for a 100% combined ratio. This suggests that the insurance market is about to become “hard”, cash flow underwriting is about to end, and premiums will rise. Better to renew your insurance coverage sooner rather than later, as later it will likely be more expensive.