New York City Sea Barriers

I had the opportunity to tour the emergency response center of New York City’ s Office of Emergency Management. Officials there told me that one of their greatest concerns was the threat of a major hurricane striking the city. Indeed, National Hurricane Center Director Max Mayfield testified before Congress “it is not a question of if a major hurricane will strike the New York area, but when.” A hurricane would flood Wall Street, the financial district, densely packed neighborhoods and the City’s infrastructure, which is largely underground, such as the subway. So I was very interested to learn of a conference held in advance of the new hurricane season (which starts on Monday) in which innovative solutions for New York were presented.

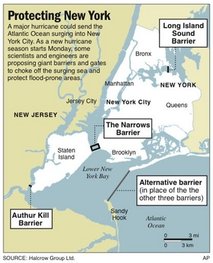

Some engineers are proposing the construction of a barrier to block the sea surges and protect areas vulnerable to flooding. One idea involves the construction of a barrier between New Jersey and Queens, some five miles long, which would rise out of the water to meet storm surges. It may sound extreme, but if New York were to experience a repeat of the hurricane that struck Long Island in 1938, the storm surge would be as high as 25 feet in parts of New York City. The result would be flooding of as many as 600,000 homes and an evacuation of three million New York residents. The economic losses would exceed $100 billion. This makes the cost of the barriers, estimated to be $6 – $9 billion, appear to be a sensible investment. Of course, at this time New York doesn’t have the finances for such an investment and seeking help from the federal government would not appear to be a prudent strategy. Surely every community would rightly demand the same protection. For the time being, it make sense to prepare for flooding by moving critical infrastructure such as pumps to higher elevation areas. It also makes sense to launch a public awareness campaign. When I toured OEM’s command center, I learned that their leadership feared New York residents would enter subway stations on a storm alert – the last place you want to be when a hurricane or flood is forecast.