This is a test.

This is a test

May 29th, 2015This is a test

May 28th, 2015This is a test.

This is a test

May 27th, 2015This is a test.

This is a test

May 26th, 2015This is a test.

Memorial Day

May 25th, 2015

Honoring Those Who Served

Today is Memorial Day and in addition to remembering those who served, we can also honor veterans by patronizing their businesses. There are three million veteran-owned businesses in the United States, as men and women bring the leadership skills they developed during their military service to become successful entrepreneurs. There are online directories to locate businesses that have been certified by the U.S. Veterans Administration as being veteran-owned. It is amazing how military service equips people to become successful with their own businesses. My home inspector is an Air Force veteran and his business is the best of its kind in the state. One of my favorite restaurants was started by a Navy veteran. So today as we remember and honor those who served, we can also support what they continue to do for us in our local communities.

This is a test

May 24th, 2015This is a test.

Environmental Metrics

May 23rd, 2015

Measuring Savings

There is an old saying that “what is measured, is managed” so I am always intrigued to see ways of measuring the impacts of small steps we can each take to reduce our environmental footprint/carbon emissions to reduce disaster impacts. This dispenser provides filtered water to employees of a Fortune 500 company. Each floor has one to encourage use. The dispenser is equipped with an automatic sensor. Once you place your refillable bottle underneath the spout, filtered water is dispensed and the small green screen at the top right of the unit tracks the number of refills as “Helped eliminate waste from 13,457 disposable plastic bottles”. The dispenser is an effective reminder of the cumulative benefits of avoiding disposable plastic water bottles that only wind up in landfills.

NuRide is another service that measures and rewards individual efforts to reduce environmental impacts. You can sign up for NuRide and use the service to find a ride-share or a car-pooling buddy. You can also create a free account and enter details of when and where you took public transportation, shared a ride with someone or walked or biked to your destination. You earn points for these efforts and they add up to rewards such as free admission to cultural events or discounts on purchases. I am trying to work out a model of how we would measure improved small business commercial resiliency measures and, in an analytically rigorous way, translate those measures into reduced premiums commensurate with better risk practices. So I find these models helpful and, of course, use both.

This is a test

May 22nd, 2015This is a test.

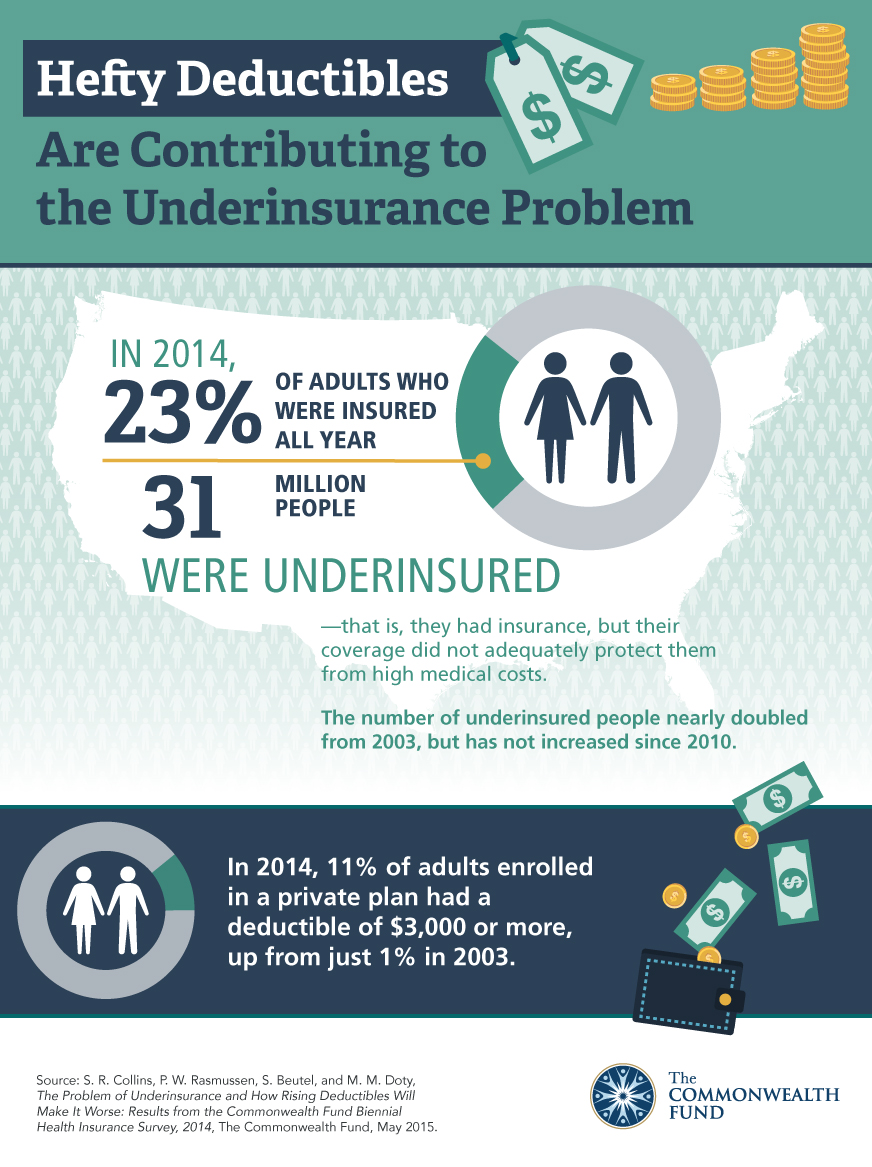

Rising Insurance Deductibles Contribute to Increase in Rates of Underinsured People

May 21st, 2015

Covered, But Still at Risk

A new report of the Commonwealth Fund finds that last year, 31 million Americans with health insurance had inadequate coverage or were underinsured. People are considered underinsured if they have had health insurance for a full year, but have high deductibles or out-of-pocket expenses relative to their income. The report found that the consequences of being underinsured are significant. Half (51%) of those who were underinsured had problems paying medical bills or were paying down medical debt over time. More than one-third (38%) were struggling to pay or could not pay their medical bills and one-third (34%) had long-term medical debt. More than one-fifth (23%) were contacted by a collections agency concerning unpaid medical bills or said that had to make lifestyle changes in order to pay their medical bills (22%). Following on the JP Morgan Chase study, cited in a recent blog entry, about the difficulties people are having with volatile income and unpredictable expenses, this study provides insight into the financial stress many Americans are suffering. Is there a way you can reduce the burden on your employees, such as through the use of tax-advantaged Health Savings Accounts? High deductibles and co-payments may discourage over-utilization, but it is counter-productive to have people deferring necessary care because of the out-of-pocket costs only to have a more serious, and more expensive medical problem later. In Prepare for the Worst, Plan for the Best: Disaster Preparedness and Recovery for Small Businesses, I recommended that small business consider reducing their commercial insurance premiums by selecting higher deductibles (and saving and budgeting for those deductibles). But for medical insurance, I favor the opposite approach.

JP Morgan Bank Study Reports Extreme Volatility in Income and Spending

May 20th, 2015Today, the JP Morgan Chase Institute released a study titled Weathering Volatility: Big Data on the Ups and Downs of U.S. Individuals from which the key finding can be summarized as (from page 5 of the study):

The typical household did not have a sufficient financial buffer to weather the degree of income and consumption volatility observed in our data. The typical household did not maintain enough liquid savings that could be accessed immediately in the event of a large, unexpected expense sustained at the same time as a loss in income. While many in the field of consumer finance have long advised that consumers maintain an emergency fund, our research into income and consumption volatility shows that a financial buffer is a more important consideration for individuals across the entire income spectrum than is generally understood. We find that not only was volatility high for income and consumption, but also changes in income and consumption did not move in tandem. This creates the risk that people might experience a negative swing in income at the same time that they incur a large, potentially unexpected, expense.

The study found that income and expenses for individual bank consumers fluctuated among all groups across the income spectrum: the relatively affluent and the less comfortable alike. While this finding is not unexpected, what is unusual is the size and scope of the data collection efforts of the JP Morgan Chase team to conduct their analysis and reach their conclusions. They considered a sample of 2.5 million out of a total of 27 million account holders of JP Morgan Chase Bank on which they analyzed 135 million financial transactions, over a 27 month period across all of the Bank’s consumer products (checking accounts, savings accounts, credit card accounts, home equity accounts, mortgage and automobile loans) and obtained corresponding account information from the credit bureaux.

I was particularly interested in the study’s statement concerning the risk that people may experience a drop in income at the same time they incur a large, unexpected expense. Of course, this is exactly what happens to small business owners when disaster strikes: they experience large expenses (uninsured losses, insurance deductibles, etc.) even as their income fluctuates until the business can recover its earnings capacity and/or customers return to the disaster zone and normal economic activity resumes. Clearly small business owners need larger reserves of savings to cushion these shocks. But often we are seeing the opposite result: dwindling savings as small businesses are covering expenses from their own reserves as capital access is constrained. Indeed, I had reported in an earlier blog post that the small business development centers in New Orleans had shared with me that the local businesses they serve lacked sufficient funds to cover the costs they would incur should an evacuation be ordered – a particularly alarming finding in hurricane season.

The study concludes with a recommendation for greater innovation to make tools and financial products available to cushion the financial shocks resulting from fluctuations in income and expenses. I don’t agree entirely with that finding. The fact is we have such products available, but the large segment of the U.S. population that lacks basic bank accounts shows there is a problem with access. Similarly, many small business owners lack adequate insurance to cover their losses. Perhaps the focus should be not on financial innovation but on expanding financial literacy to inform people of financial solutions currently available to them.